Navigating the South African Car Market: A Guide for Young Professionals

Navigating car ownership in SA? Get clear answers on balloon payments, used vs. new vehicle depreciation, the 50/30/20 budget rule, and hidden costs.

The excitement of buying your first (or second) car is a major milestone in your professional journey. However, in the 2026 South African economy—characterized by a cooling inflation rate of 3.6% and prime interest rates stabilizing around 10.25%—the "new car smell" can quickly be replaced by financial stress if the math doesn't "math".

As Elisma highlighted in our recent video, buying a car isn't just about the monthly installment, it's about how that asset fits into your long-term Financial Foundations. Here is an exhaustive guide to navigating this complexity with confidence.

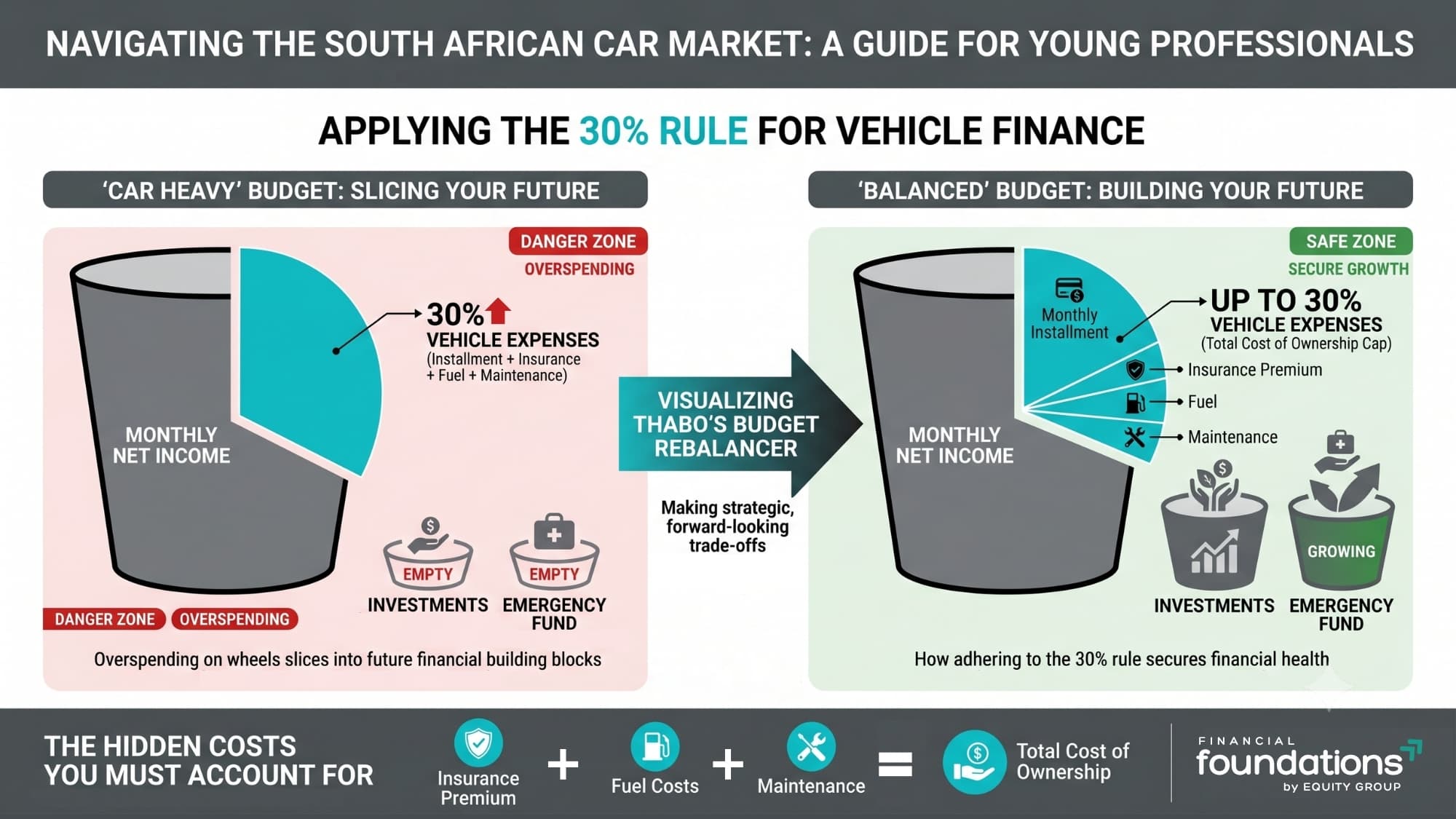

@financialfoundations47 2026 vibes... 🚗💨 Before you sign those vehicle finance papers, let's look at the real cost of buying a car. 📝 If your monthly car expenses take up more than 30% of your take-home income, your budget is officially in the danger zone 🚨. And no, that 30% doesn't just mean your installment. It has to cover insurance, fuel, and maintenance too 💸. When you overspend on wheels, you slice right into the money that should be building your future bucket 📉. Navigating car buying doesn't have to be complex. Keep your cash flow secure with digestible, expert strategies 🛠️. #FinancialFoundations #carbuyingtips #Budgeting101 #YoungProfessionals #SouthAfrica #PersonalFinance #fypp

♬ original sound - Elisma Fourie - Elisma Fourie

1. Anchoring Your Choice in the 50/30/20 Rule

Before you step onto a dealership floor, you must understand where a car sits in your budget. At Equity Group, we recommend the 50/30/20 rule as your North Star:

- 50% for Needs: This includes your car installment, insurance, and fuel.

- 30% for Wants: Lifestyle and hobbies.

- 20% for Your Future: Savings, debt repayment, and investments.

The Trap: Many young professionals view a car as a "Need" but choose a model that pushes their "Needs" bucket to 70% or 80% of their income, effectively "starving" their future self. If your car costs more than 15-20% of your total take-home pay, you are likely overextended.

2. New vs. Pre-Owned: The "Sweet Spot"

In 2026, the used-to-new vehicle financing ratio in South Africa has climbed to 1.56:1, meaning for every new car financed, nearly two used ones are sold.

- The 3-5 Year Rule: To avoid the heaviest blow of depreciation, aim for vehicles between three and five years old. By this stage, the original owner has already absorbed the rapid value loss, but the car is often still modern enough for decent safety features.

- The Average Entry Point: The average financed pre-owned purchase in early 2026 is approximately R396,000.

- Entry-Level New: If you value peace of mind, 2026 entry-level models like the Suzuki S-Presso or Renault Kiger are aggressively priced to compete with used options and come with full warranties.

3. Decoding the "Balloon Payment" Trap

A balloon payment (or residual value) is essentially a lump sum deferred to the end of your loan term. While it makes monthly installments look attractive, it comes with significant risks:

- How it works: If you buy a R400,000 car with a 20% balloon, your monthly payments only cover R320,000 of the capital. However, you pay interest on the full R400,000 for the entire term.

- The Final Bill: At the end of your term (e.g., 72 months), you will owe a lump sum of R80,000.

- The Risk: If you haven't saved for this, you may be forced to refinance it (paying more interest) or have the car repossessed if you cannot settle the debt.

4. The "Real" Monthly Cost of Ownership

Your bank statement will show more than just an installment. A realistic 2026 car budget must include these "hidden" costs:

- Insurance: Expect to pay between R500 and R2,000 monthly, depending on your age and the vehicle's value. Always include shortfall cover to protect against a balloon payment if the car is written off.

- Fuel: For a compact hatchback driving 1,000km a month, budget at least R2,000.

- Maintenance: Set aside R500 a month (or 10-15% of the car's value annually) for tires, brake pads, and servicing if the car doesn't have a service plan.

- Admin Fees: Don't forget the once-off finance admin fee (roughly R1,200) and the monthly bank admin fee (around R69).

- Annual Licensing: A small hatchback costs around R600 per year for a new license disc.

5. Strategy: Walk in as a "Cash Buyer"

One of the most powerful moves a young professional can make is getting pre-financing approved before visiting a showroom.

- Bargaining Power: Pre-approval gives you the status of a "cash buyer" in the eyes of the salesperson, preventing them from talking you into in-house financing with higher rates.

- Credit Health: Your interest rate is directly tied to your credit score. Use the Equity Group Financial Health Tool to check your status before applying for a loan.

6. The Multi-Domain Professional Perspective

As we've seen with cases like Thabo, who uses his skills to generate multiple income streams, a car should be a tool that enables growth, not a burden that hinders it.

- If a car allows you to reach clients for a side hustle (poly-jobbing), it can be a Brand Multiplier.

- However, if the costs prevent you from investing in the learning phase of a new skill, it is a liability that delays your financial independence.

Ready to start your journey?

Explore our interactive tools to see how your financial decisions today impact your future:

- Try the 50/30/20 Budget Rebalancer to see if your dream car fits your reality.

- Financial Health Tool: Assess your overall financial standing in minutes.

- Investment Growth & Volatility Tool: Visualize how consistent saving overcomes market noise.

- Retirement Nest Egg Predictor: See how your "Future bucket" grows over time.

Frequently Asked Questions: Buying a Car in South Africa (2026)

1. Is a balloon payment a good idea for a first-time car buyer?

While a balloon payment (residual value) lowers your monthly installments, it is essentially "debt delay." In the South African context of 2026, you pay interest on the full value of the car, including the balloon amount, for the entire loan term. Unless you have a disciplined savings plan (like an automated investment account) to settle the lump sum at the end, you risk having to refinance the debt at a higher total cost or losing the vehicle.

2. How much of my monthly salary should I realistically spend on a car?

Following the 50/30/20 rule, your total "Needs" (housing, food, and transport) should not exceed 50% of your take-home pay. Specifically for car ownership, experts recommend that your installment stays below 10% of your net income, and your total cost of ownership (installment + fuel + insurance + maintenance) stays below 20%. If you are a "Multi-Domain Professional" with side income, use that surplus to reduce the loan principal rather than buying a more expensive model.

3. Is it better to buy a brand-new car or a 3-year-old used vehicle in 2026?

The "sweet spot" for value in 2026 remains the 3-to-5-year pre-owned market. A new car loses roughly 15–20% of its value the moment it leaves the floor. By buying a 3-year-old vehicle, you let the first owner pay for that depreciation while you still benefit from modern safety features and, often, the tail-end of a factory service plan. With the 2026 used-to-new financing ratio at 1.56:1, the pre-owned market offers significantly more variety for your budget.

4. Can I use my "Two-Pot" retirement savings to settle my car loan?

With the retirement reforms that took effect in 2024, you can access your "savings pot" once per tax year. While some young professionals use this to settle high-interest car debt, remember that these withdrawals are taxed at your marginal tax rate (your normal income tax bracket). It is generally more effective to use these funds only for emergencies and to focus on "poly-jobbing" or side hustles to pay down car debt faster without sacrificing your future compound interest.

5. What "hidden costs" of car ownership should I include in my budget?

A common mistake is budgeting only for the bank installment. In South Africa, you must factor in:

- Comprehensive Insurance: Non-negotiable if the car is financed (approx. R800–R2,000 pm).

- Maintenance Fund: At least R500 pm for tires and wear-and-tear parts not covered by service plans.

- Fuel Volatility: Budget at least R2,000 pm for an average 1,000km commute.

- Annual Licensing: Approximately R600 per year for your disc renewal.

Sources:

- AutoTrader: Top tips for buying a car on a budget in South Africa (2026)

- WesBank: Buying a Used Car in 2026? Here's What South Africans Should Know

- SARB: Statement of the Monetary Policy Committee January 2026

- Nedbank: How vehicle finance with a balloon payment works

- Nedbank: The real costs of owning a car in South Africa

- Image source: https://www.cars.co.za/motoring-news/which-new-cars-can-you-buy-for-r5k-a-month-in-south-africa/337415/